The Impending End of the National and Public Health Emergencies and Its Effect on Health and Welfare Plans

May 8, 2023 - Alerts by Hinkle Law Firm

On January 30, 2023, President Biden issued the long-anticipated announcement that the COVID-19 national and public health emergencies will end soon. (Yes, two different “emergencies” are currently in effect, with different consequences flowing from each, but the distinction between them is not important for our purposes.) According to the official Statement of Administration Policy, the public health emergency and national emergency are set to expire on May 11, 2023. However, Congress took matters into their own hands with respect to the national emergency and passed legislation, which the President signed, that ended the national emergency on April 10, 2023.

To read this Alert in PDF format, click here.

Impact of the Emergencies on Group Health Plans

The main impact of these two “emergencies” on group health plans offered by employers to their employees is as follows:

• Certain deadlines have been extended for as long as an additional year; and

• Plans have been required to provide coverage for COVID-19 testing and vaccines.

See our May 11, 2020 Alert for more details.

For the last three years, these changes have become the new normal for employers and plan administrators. The end of the emergencies will finally bring an end to most of these temporary mandates. This Alert is intended to help prepare plan sponsors and administrators for this transition.

Extension of Deadlines

In response to the COVID-19 national emergency, the Department of Labor, Department of the Treasury, and the IRS issued joint relief, effective March 1, 2020, that extended the timeframes for an array of health and welfare plan actions, including the following:

- Exercising HIPAA special enrollment rights;

- Providing COBRA notices, electing COBRA continuation coverage, and paying COBRA premiums;

- Filing claims and appeals of adverse benefit determinations; and

- Requesting external review after an adverse benefit determination.

The relief provided by these agencies states that the timeframes for each of these actions are extended during the “Outbreak Period.” The “Outbreak Period” is defined as the earlier of (i) 60 days after the end of the national emergency or (ii) one year from the date of the original deadline. Because the national emergency ended on April 10, 2023, the extension of these timeframes will thus expire no later than June 9, 2023 (i.e., 60 days after the end of the national emergency). After that, each of the extended timeframes will revert to their original deadlines. To add even more confusion, the Department of Labor issued informal guidance indicating it still considers July 10, 2023 as the end of the Outbreak Period. Clear as mud, right?

Examples Illustrating the Extension of Normal Deadlines

To help you navigate between the pre-Outbreak Period rules, the extension of the same due to the Outbreak Period, and the transition back to normalcy, consider the following hypotheticals involving COBRA elections. Despite the uncertainty regarding when the Outbreak Period actually ends, assume it will end on June 9, 2023, for purposes of these hypotheticals:

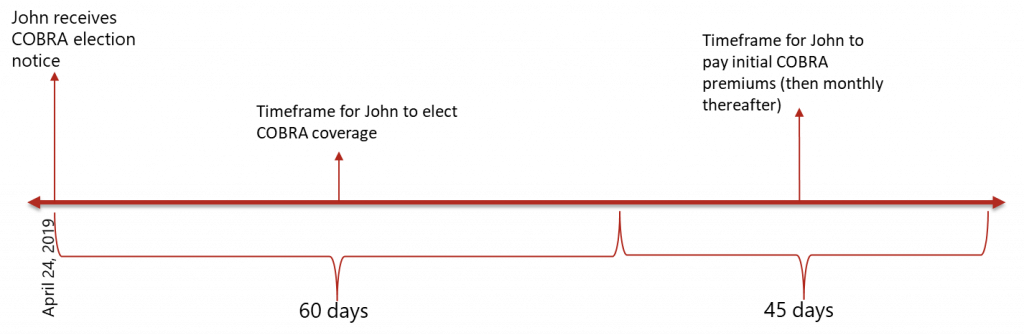

- John is a participant in the Acme Corp. Medical Plan. On April 24, 2019, his employment with Acme was terminated, and he lost his eligibility for coverage that same day. This termination represented a COBRA-qualifying event, and Acme provided a COBRA election notice to him at the end of the day. The following graphic provides a snapshot of the COBRA timeframes under the pre-Outbreak Rules.

- Now, assume John’s employment terminated during the Outbreak Period. That is, his employment with Acme terminated on April 24, 2020, and he lost his eligibility for coverage that same day. The termination was a COBRA-qualifying event and, once again, Acme provided him a COBRA election notice at the end of that day. By virtue of the suspension of deadlines pursuant to the national emergency, his time for returning that election notice was substantially expanded. The following graphic provides a comparison of the original rules (red) against the Outbreak Period extension (blue). As noted in this example, the Outbreak Period provided an opportunity for participants to wait to see if they incurred significant claims before electing COBRA.

- Finally, assume John’s employment and coverage were terminated on April 24, 2023. He received a COBRA election notice that same day. Once the Outbreak Periods ends on June 9, 2023, the clock on his deadline for making his COBRA election will begin ticking again. The following graphic compares the original rules (red), the Outbreak Period extension (blue), and when John must elect COBRA once the national emergency ends (green).

In anticipation of this transition, plan sponsors and administrators should ensure their plan documents and COBRA notices account for the end of the Outbreak Period. As much clarity as can be provided as to the exact deadline for participants to make elections and pay premiums will serve everyone well. Additionally, it may be beneficial to provide a notice to participants summarizing the upcoming changes.

Required Coverage for COVID-19

Switching gears, in addition to the end of the national emergency’s effect on deadlines, the end of the public health emergency will affect certain substantive coverage mandates. During the public health emergency, plans were required to cover COVID-19 diagnostic and preventive care services, including tests and vaccines.

The coverage that was required for the diagnosis of COVID-19 developed as follows:

- Beginning March 18, 2020, the Families First Coronavirus Response Act required all public and private insurance coverage, as well as self-funded plans, to cover COVID-19 tests, and costs related to diagnostic testing, with no cost sharing for the duration of the public health emergency.

- This was later expanded by the Coronavirus Aid, Relief, and Economic Security (CARES) Act to cover out-of-network tests during the public health emergency.

- The Consolidated Appropriations Act of 2021 again expanded this requirement to over-the-counter COVID-19 tests.

- The Departments of Labor, Health and Human Services, and Treasury later issued guidance requiring health plans to cover up to eight free over-the-counter at-home tests per covered individual per month or provide tests through participating network providers. This requirement became effective January 15, 2022.

Additionally, under the CARES Act, non-grandfathered plans are required to provide first-dollar coverage for all COVID-19 preventive items, services, and immunizations receiving specified recommendations from the CDC. This includes any COVID-19 vaccine authorized under an Emergency Use Authorization or approved under a Biologics License Application by the FDA.

When the public health emergency ends, plans will no longer be required to provide first-dollar coverage for the above-described diagnostic services. However, plans must continue to cover in-network, recommended COVID-19 vaccines without cost sharing.

In anticipation of these changes, plans should decide whether they want to continue providing first-dollar coverage for diagnostic services when it’s no longer required. At this time, it is not clear what notices, if any, are required to be provided prior to discontinuing coverage for diagnostic services.

We hope this information is helpful. If you have any questions about how the end of the national emergency and public health emergency affects your health and welfare plans, please do not hesitate to contact one of the following attorneys on our Employee Benefits team at (316) 267-2000.

To read this Alert in PDF format, click here.

Employee Benefits Attorneys

Eric Namee

Steven Smith

Brad Schlozman

Blair Bohm